Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

Last Updated on: 2nd April 2025, 10:18 am

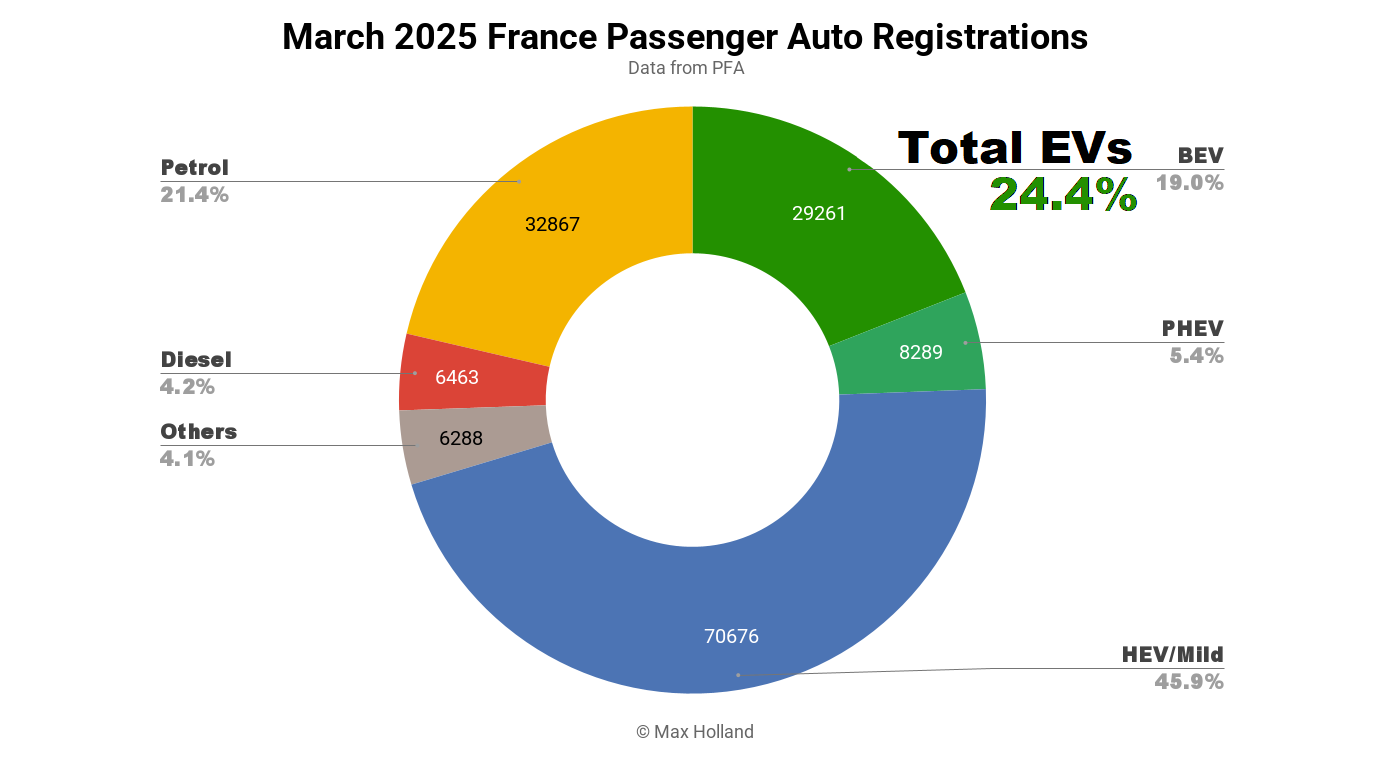

March’s auto sales saw plugin EVs take 24.4% share in France, a drop from 27.9% year-on-year. The YoY baseline was elevated by a pull-forward ahead of incentive cut-offs, so the YoY comparison is temporarily skewed. On a normalized basis, BEVs continue to climb, albeit slowly. PHEVs are down YoY due to being newly subjected to weight-based taxes in 2025. Overall March auto volume was 153,844 units, down over 14% YoY. The Renault 5 was once again the best selling BEV in March, consolidating its popularity.

March’s auto sales totals saw combined plugin EVs take 24.4% share in France, with 19.0% full battery-electrics (BEVs) and 5.4% plugin hybrids (PHEVs). These compare with YoY figures of 27.9% combined, 18.9% BEV and 9.0% PHEV.

As alluded to above, the YoY baseline for BEVs was distorted by a March 2024 pull-forward of sales of a number of popular BEV models. This was a late rush to grab the purchase incentive ahead of a mid-March cut-off for pretty much all BEV models manufactured outside the EU. Popular models like the Tesla Model 3, Dacia Spring, Kia Niro, MG4, Nissan Ariya, and many others were affected.

If we take a step back, however, 2025 has seen a slow but steady increase in BEV market share from 17.4% in January, to 17.9% in February, to 19.0% now in March. The cumulative year-to-date share now stands at 18.2%. As mentioned in recent reports, the planned 2025 EU-zone emissions regulations were likely to imply a zone-wide share of between 20% and 22% for BEVs, with France expected to achieve something close to the zone-wide average.

In early March 2025, however, EU Commission president Ursula von der Leyen decided to loosen the full year 2025 vehicle emission targets. Put simply, the proposed loosening essentially allows the 2025 target to now be pooled with the 2027 targets, instead of conforming to the previously planned step-by-step tightening in each intermediate year. At the same time, von der Leyen announced an 800 billion euro “ReArm Europe” plan, including scrapping previous government fiscal limits, to encourage prioritising public and private focus and investments towards the buildout of military production capacity, at a scale not seen since the 1940s. If this goes ahead, it will potentially have the opposite result for EU climate progress, as militaries typically have the heaviest climate emissions of any organization.

The proposed vehicle emissions loosening will likely disrupt the emerging trajectory of 2025 BEV growth in France (and in the wider EU region). On the other hand, somewhat affordable small-and-competent BEVs now exist in the European market, due to the previously planned rules (before the March 2025 change of direction). Put simply — the cat is already out of the bag, in the form of the Citroen e-C3, the Renault 5, the Hyundai Inster, and many others. Will consumers who have made plans “at long last” to buy these kinds of BEVs in the coming months now switch their attention back to ICE-powered vehicles? Let me know in the comments.

The good news as of the March results is that, mainly thanks to their being substituted by HEVs and MHEVs, ICE-only powertrains were down significantly in YoY volume and share. Diesel-only volume fell from 13,532 units to 6,463 units, and to a record low share of 4.2%. Petrol-only volume fell from 58,895 down to 32,867, and share fell to 21.4% — also a record low.

France’s Best Selling BEV Models

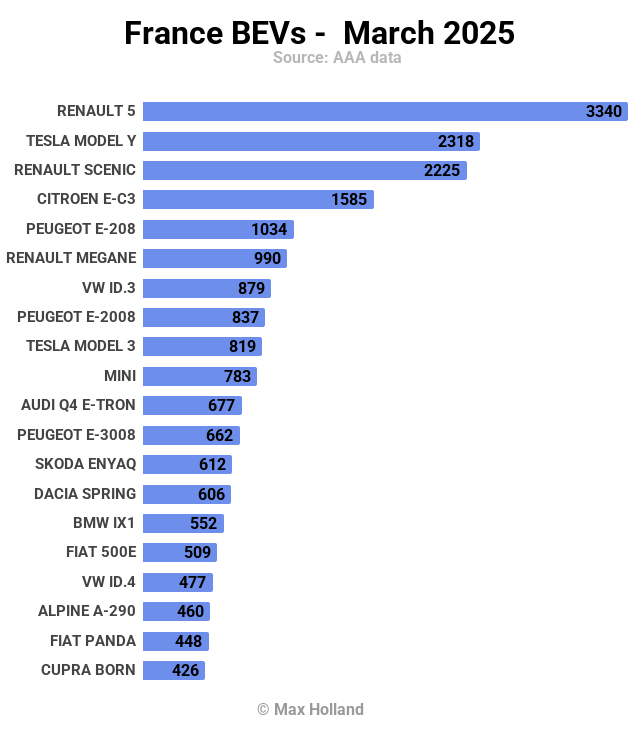

The Renault 5 was once again France’s best selling BEV model in March, with 3,340 units registered. This is its third pole position in the past five months (and in the other two months, it placed second)!

In the runner-up position was the Tesla Model Y, with 2,318 units registered, some of which are likely the refreshed version.

In third was the Renault Scenic, with 2,225 units.

The top 5 were all the same faces as last month, with just some minor shuffles of position.

In fact, besides regular month-by-month variations, the only major change in the top 20 ranking was the addition of the new Fiat (“Grande”) Panda, which joined for the first time, in 19th, selling 447 units. Due to limited data, we can’t say for sure when the Panda debuted in the French market (chime in if you know), but it is clearly off to a decent start.

The diminutive Panda has a length of 3,999 mm (slightly shorter than its cousin, the Citroen e-C3), and has an MSRP starting from €23,253 in France. This is yet another of the new small BEVs from Stellantis (Opel, Frontera, Citroen e-C3/Aircross) which sit on the electrified CMP platform.

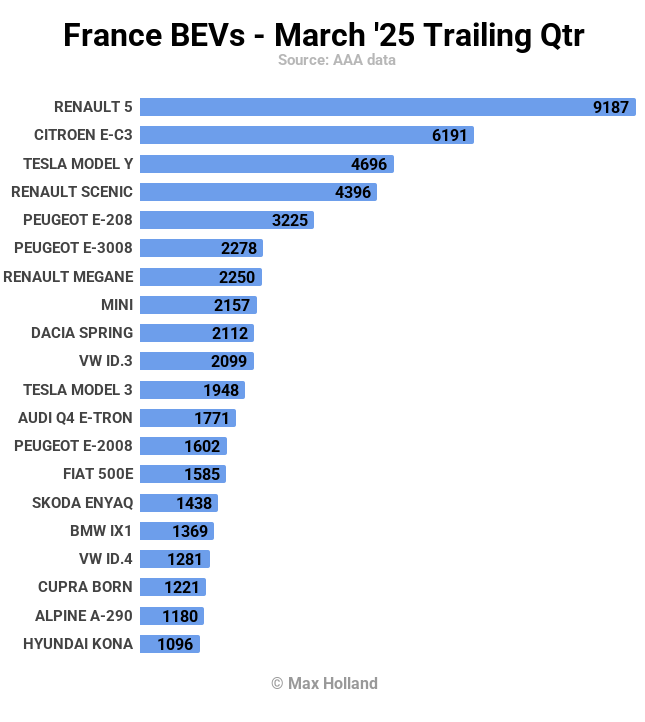

Let’s now turn to the 3-month chart:

Here the Renault 5 maintains its recent dominance, and with its 3rd straight month in the top spot (having only narrowly missed out to the Tesla Model Y in December). Considering the Renault only hit its volume stride in November, this is a great result, and indicative of the latent demand for small-and-competent BEVs.

That latent demand is reinforced by the Citroen e-C3 taking the second spot, and having been in the top 3 spots consistently for the past 7 months, ever since its own September 2024 debut.

Based on this trend, within a couple of years, the top 20 BEVs will potentially become dominated by B-segment and smaller classes, much as the broader French auto market has traditionally been. This probably means a median battery pack size of 45 to 50 kWh — which is an efficient use of resources. A similar pattern may hold for much of southern Europe in the long run.

Outlook

Ten out of twelve of the past months have seen YoY contraction of France’s auto sales (by an average of 6.5% YoY). The broader French economy continues along at only modest GDP growth of just 0.6% in Q4 2024 (latest data), with a current forecast of around 0.7% to 0.8% YoY for each quarter of 2025.

Inflation is currently at 0.8%, and interest rates stand at 2.65%. Manufacturing PMI improved in March to 48.5 points (the highest in two years), from 45.8 in February.

After being delayed in the planning pipeline for several years, somewhat affordable BEV offerings are now coming available in Europe, including in the small-and-simple vehicle classes traditionally favoured in the French market. With these now “known about” by prospective new car buyers, it’s hard to see how the cat gets put back in the bag at this stage.

With the EU commission’s backpedalling on 2025 emissions, even if legacy auto manufacturers slow down the availability of these affordable models, are consumers really going to switch to an ICE vehicle instead of waiting a bit longer to get their BEV, or perhaps turn to brands (BYD, Hyundai, others) which won’t take part in this backpedalling?

What do you think about France’s transition to EVs? Will the recent backpedalling on emissions regulations lead to yet another year of lost progress, or is the momentum and latent demand too strong at this point to hold back the transition any longer? Please share your thoughts and comments in the discussion below.

Whether you have solar power or not, please complete our latest solar power survey.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy