Sign up for daily news updates from CleanTechnica on email. Or follow us on Google News!

EVs Now 19% of World Auto Sales

Global plugin vehicle registrations were up 49% in February 2025 compared to February 2024. There were 1.2 million registrations. More good news is that BEVs pulled further ahead of plugin hybrids, growing 58% YoY to 814,000 units compared to plugin hybrids growing 35% to some 403,000 units in the same period.

Interestingly, not only are plugins growing, but fossil-fueled vehicle sales, including plugless hybrids, are on the way down, having fallen some 8% YoY in February.

In the end, plugins represented 19% share of the overall auto market (13% BEV share alone). This means that the global automotive market remains firmly on the path to electrification.

Year to date, plugin electric vehicle market share is also at 19% (13% BEV), thanks to a healthy 32% growth rate. And this isn’t just the result of the quick electrification process of the Chinese automotive market, because even if we exclude China from the total tally, plugins are still growing by 26% YoY, with the major difference being that PHEVs see their growth rate fall from 20% with China included to just 6% if we exclude the largest automotive market in the world.

Significant growth is happening not only in China but also in North America (+20%), Europe (+19%), and especially in the Rest of the World (+35%). The biggest growth is mostly coming from Asia — Indonesia (+205%), Vietnam (+220%), and Singapore, for example. This last case is especially interesting, because the small country is more than doubling its EV sales from an already significant base in 2024. In fact, it is now at 42% EV share in 2025.

At this pace, not only will Singapore have its automotive market fully electrified before the end of the decade, but it could be the second automotive market, after Norway, to be fully electrified. It could surpass not only China, but also heavily electrified markets like Iceland and Denmark.

Full electric vehicles (BEVs) represented 67% of plugin registrations in February, pulling the year-to-date tally slightly up, to 66% share. 2024 finished with a 63% share for BEVs, so 2025 is turning out to be a positive year for pure electrics in this metric, too.

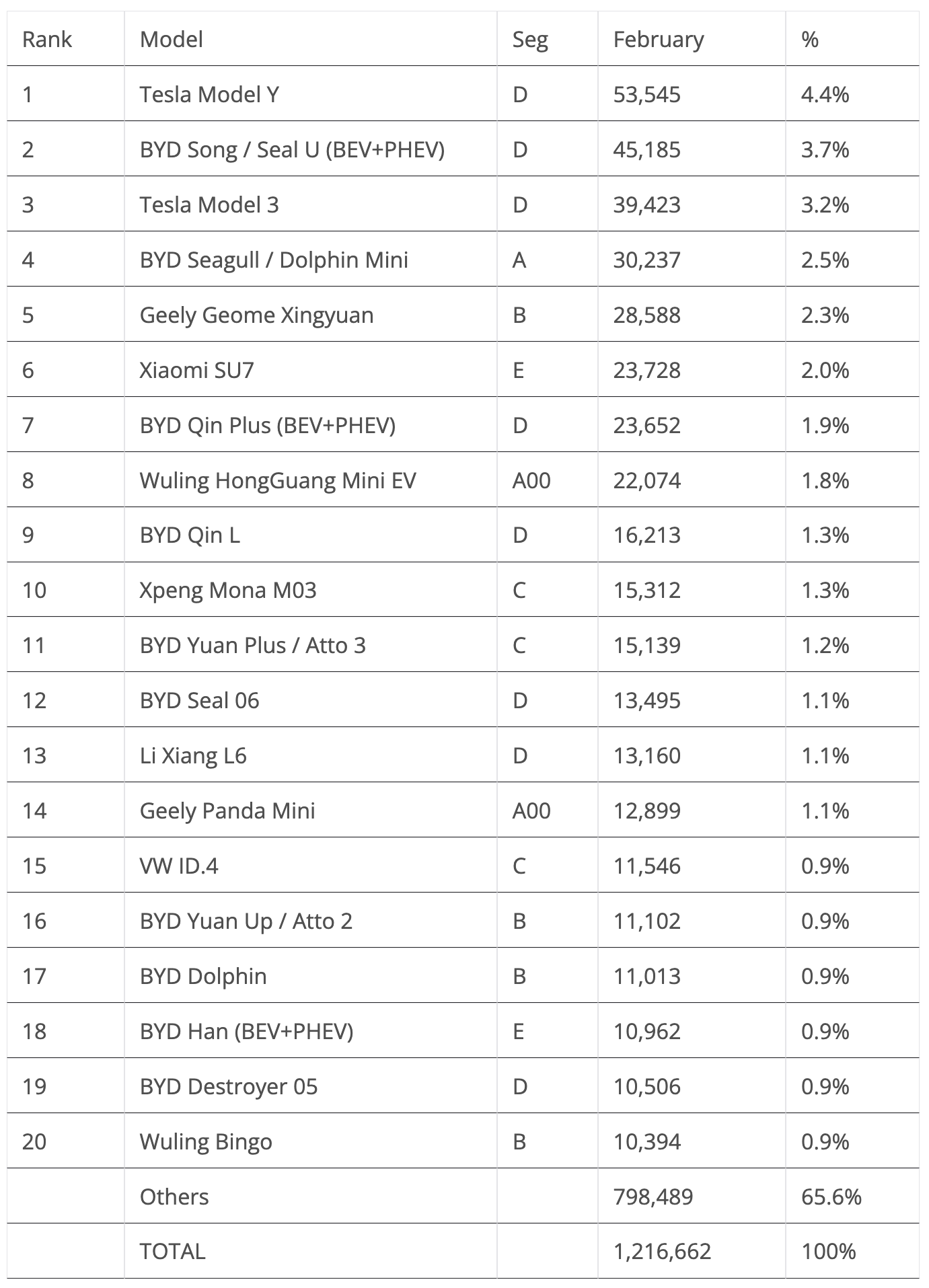

20 Best Selling EV Models in the World in February

Back to February’s best sellers. While the Tesla Model Y was in the lead, its monthly tally, some 54,000 deliveries, was down by 28% YoY. With the refreshed units landing in March, expect the numbers to recover then.

Still on Tesla, the Model 3 ended the month in 3rd, thanks to some 40,000 registrations. Surprising good news is that the sedan’s deliveries increased by 18% YoY, thus helping to compensate for the Model Y’s sales blues.

As for BYD, the Shenzhen make placed the Song in the runner-up spot, between both Teslas. The little Seagull ended in the 4th position, with over 30,000 deliveries, and … eight other BYD models made it into the top 20. I won’t bother mentioning them all — that’s a lot of BYDs….

Talking about models not named Tesla or BYD, the highlight is the small Geely Geome Xingyuan, which delivered another record performance, 28,588 registrations. That allowed it to end the month in 5th, and win the title of the best NBT (Non-BYD/Tesla). The car has been a welcome surprise, and it could have a bright future in export markets. The question is, is Geely willing to market it outside of China?

Another highlight this month was the continued success of the Xiaomi SU7, a Model S–sized car that somehow resembles a Porsche and yet costs Model 3 money. With over 23,000 registrations, it ended the month in 6th. With the sporty sedan still limited to its domestic market, one wonders how many more units it will be able to sell in export markets, once available. Once it crosses Chinese borders, will this be the Tesla Killer best selling sedan in the world?

Elsewhere, a mention also goes out to Xpeng’s Mona M03, which had over 15,000 deliveries in February. The success of this liftback-that-looks-like-a-sedan is crucial to the startup’s path to profitability, which sits on the horizon of the Chinese OEM — but how far on the horizon is unclear.

Still on the top 20, a final mention goes out to Volkswagen’s ID.4. The German crossover reached #15 with some 12,000 registrations, and was the only legacy OEM model on the table.

Off the table, the highlight comes from the Kia stable, with the recently introduced EV3 hitting a record 8,125 registrations. With deliveries stabilizing in Europe, the compact crossover could profit from an introduction in the US market to expand sales and reach a top 20 position. Oh, wait….

Another model shining was the Changan Lumin, with 10,383 sales. It was just 11 units from a table position.

Top 20 EV Models YTD

In the year-to-date (YTD) table, the Tesla Model Y and BYD Song continue firm in the top positions, while the Tesla Model 3 profited from a better performance in February and returned to the 3rd position.

Interestingly, the podium positions at the end of February replicate the 2024, 2023, and 2022 final standings, with the Tesla Model Y on top, followed by the BYD Song and Tesla Model 3. Considering the current trends, it doesn’t seem like there will be major changes to the podium by the end of the year, so 2025 will be the 4th year in a row with the same podium standings. Boooring….

The next position change happened in 5th, with the BYD Seagull climbing two positions to 5th while two other BYDs were also on the rise, with the Qin L going up to #9 and the Yuan Plus jumping to #12.

Still on the BYD stable, we should highlight two new representatives on the table, with the Song L joining the table in #19 and the Destroyer 05 in #20. So, BYD has 9 representatives in the top 20, which might sound like a lot, until you realise that BYD has some 900 different models available. … So, it could be worse.

Elsewhere, Xpeng’s Mona M03 continues on the rise, with the big-booted compact car jumping four positions to 10th. Also, thanks to a strong month, the Wuling Bingo climbed two positions to 18th.

Looking at things from another perspective, there are as many D-segment models (10) as there are from the other segments in the top 20. As for the remaining segments, its all evenly balanced, with three A-segment representatives, two B-segment, three C-segment, and two E-segment.

Interestingly, all segment leaders belong to different brands (A — BYD; B — Geely; C — Xpeng; D — Tesla; E — Xiaomi), which is a good sign of balance.

Top Selling Brands

In February, #1 BYD, now in full export mode, got 22% of its sales from overseas markets, a stark contrast to the 10% achieved in the whole of 2024. It scored some 310,000 registrations, and with sales at this level already, one starts to wonder how high the Shenzhen make’s sales could go!

With BYD’s sales targets in 2025 set to 5.5 million units, 0.8 million of which in export markets, where will BYD stop? Ain’t no mountain high enough for BYD? Will the Shenzhen OEM dethrone Toyota as the biggest automotive group before the end of this decade? Now, that would be news….

As for Tesla, it is still in red. The 98,000 registrations represent a 13% drop compared to the same month last year. Expect March to be much better than February, not only because it is a peak month, but also because the refreshed Model Y will be landing then. But … will it be able to beat the 167,000 units of March 2024? Doubtful, considering current trends. It will already be a victory if it gets close to that result.

Still, expect Q2 to go much better, and maybe even get a couple of growth months, thanks to the full deployment of the Model Y. The problem will be afterwards, once the refresh sales bump is gone, and especially if geopolitics continue to disfavour Tesla.

Below the top two, Geely continues riding high in its quest to challenge BYD’s domination and surpass Tesla on the way. With a strong portfolio of models in China, Geely now needs to start exporting in high volumes in order to keep up the pace of BYD.

Wuling was 4th, but far from #3 Geely’s result (77,000 units vs. 43,000), so the SAIC brand best watch behind its back, as #5 Volkswagen might surprise it soon. The strong start of the year of the German brand is rather surprising, and makes one wonder if the EU’s 2025 CO2 rules had something to do with that….

Xpeng was the best selling startup, in 7th, with over 30,000 units delivered, beating #8 Li Auto, #9 Leap Motor, and #10 Xiaomi, with these four startups proving to be a Gang of Four that are beating not only foreign legacy OEMs, but also most of the Chinese legacy automakers.

Speaking of legacy brands, Kia had a strong month thanks to the success of its new EV3, while Ford managed to win a top 20 presence, in #19, something that doesn’t always happen.

A final mention goes out to the Vietnamese automaker VinFast, which shows up for the first time on the table in #20 with almost 15,000 units. That’s mostly thanks to its domestic market, which is responsible for 85% of its sales, but we should also highlight promising results in Indonesia, Malaysia, and the USA. So … it is a brand worth keeping an eye on.

In the YTD table, there wasn’t much to report at the top. BYD is well ahead of everyone else, while #2 Tesla gained a bit more ground over Geely, and with a peak in deliveries happening in March, the US brand should be safe in its position at the end of the first quarter.

Far below the podium, #4 Wuling has enough distance from #5 Volkswagen and #6 BMW to continue cruising along.

Xpeng is the best selling startup, in 7th, followed by #8 Li Auto and a rising Leap Motor, now in 9th.

Mercedes and Xiaomi benefited from a slow month from Deepal to climb one position, with the German make now in 11th, immediately followed by the hot selling Chinese startup.

In the second half of the table, the Koreans and Audi were also on the way up, with Kia now in 15th, Hyundai in 16th, and Audi in 17th.

Finally, we witness the return of Aion to the table, in #18, after a horrible start of the year, where it was left out of the top 20.

Top Selling OEMs for EV Sales

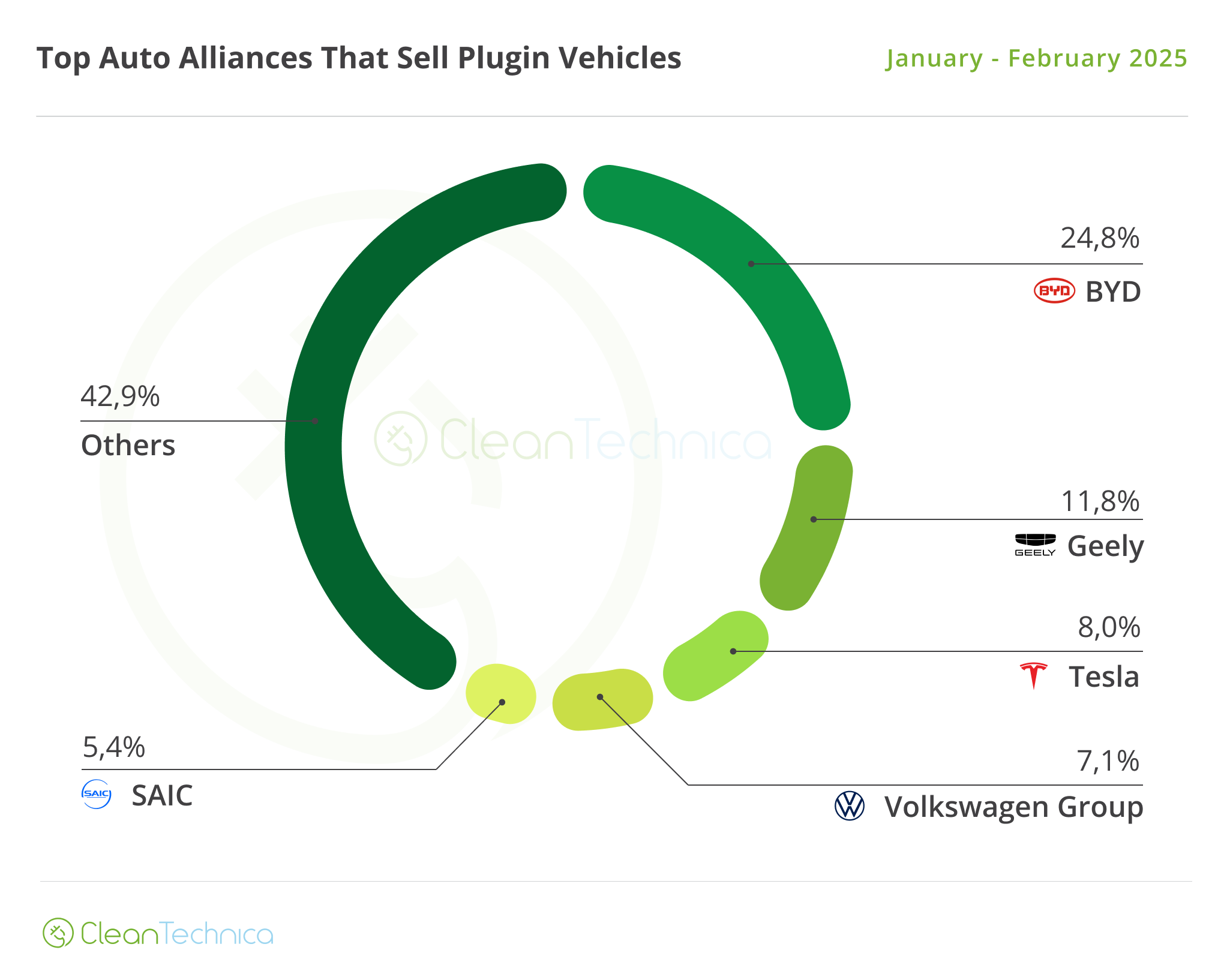

Looking at registrations by OEM, #1 BYD gained share, going from 23.6% to its current 24.8%, while #2 Geely was stable, at 11.8%, and #3 Tesla remained at 8% share.

4th place is in the hands of Volkswagen Group, with 7.1% share, a 0.1% drop compared to January. #5 SAIC is also comfortable, in the 5th position. Although, its share has dropped slightly from 5.5% in January to its current 5.4%.

BMW Group (3.6%) surpassed Chery and returned to its usual 6th position, ahead of #7 Chery and #8 Changan.

Looking just at BEVs, the big news is that Tesla (12.2%) was up one position, climbing to second with a 2,000-unit advantage over #3 Geely (12%). But even with a peak month expected in March, it will be difficult for the US brand to dethrone the current leader, BYD (15.3%), which is fast becoming the new reference in the EV world. (Tesla? That is sooooo 2020….)

In 4th we have Volkswagen Group (8.1%), which is benefiting from a strong start of the year to keep #5 SAIC (6.9%) at bay.

Hyundai–Kia also had a good month, rising from 3.7% to 3.9% share, allowing it to climb to 6th and keeping #7 BMW (3.7%) and #8 Xpeng (3.7%) at a safe distance.

Whether you have solar power or not, please complete our latest solar power survey.

Chip in a few dollars a month to help support independent cleantech coverage that helps to accelerate the cleantech revolution!

Have a tip for CleanTechnica? Want to advertise? Want to suggest a guest for our CleanTech Talk podcast? Contact us here.

Sign up for our daily newsletter for 15 new cleantech stories a day. Or sign up for our weekly one if daily is too frequent.

CleanTechnica uses affiliate links. See our policy here.

CleanTechnica’s Comment Policy